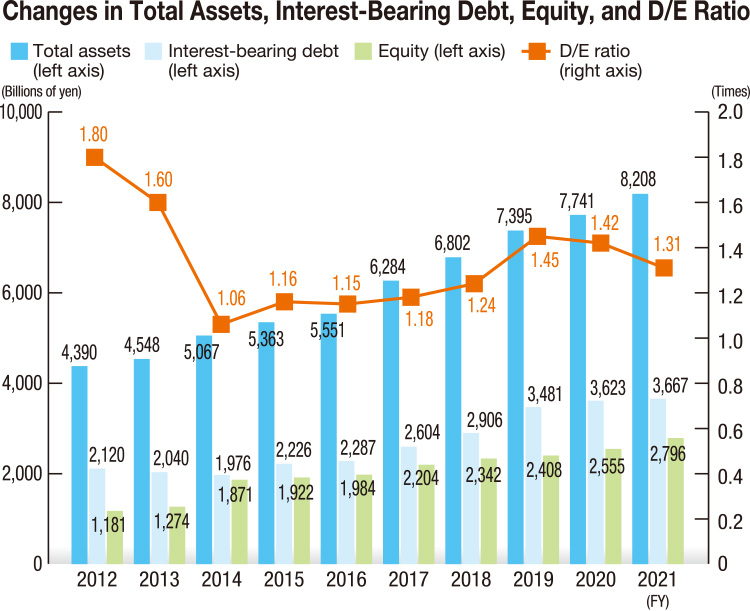

In fiscal 2021, although the COVID-19 pandemic situation continued, compared with the previous fiscal year, there was a recovery in the retail facilities' leasing business, growth in property sales to investors and an increase in revenues and profits from the Repark car park leasing business and Rehouse (retail residential brokerage). For these and other reasons, we recorded revenue from operations of ¥2,100.8 billion, operating income of ¥244.9 billion, ordinary income of ¥224.9 billion and profit attributable to owners of parent of ¥176.9 billion. Total assets on the balance sheet were ¥8,208.0 billion, an increase of ¥466.0 billion from the end of the previous fiscal year. Consolidated interest-bearing debt was ¥3,667.2 billion and net assets were ¥2,913.7 billion. As a result, the debt/equity ratio was 1.31 times and the equity ratio was 34.1%. Regarding shareholder returns, the annual dividend per share was ¥55, and the total shareholder return ratio was 46.6% due to the decision to repurchase ¥15 billion worth of shares on top of the already acquired ¥15 billion in shares.

Outlook for Fiscal 2022 Business

In fiscal 2022, while social and economic activities have been increasingly normalized with infections under ongoing control, we continue to expect COVID-19 to have an impact on the hotel and resort business. However, taking into account the recovering business performance of retail facilities and Tokyo Dome and including contributions from newly completed office buildings, among others, we forecast revenue from operations of ¥2,200 billion, operating income of ¥300 billion, ordinary income of ¥260 billion and profit attributable to owners of parent of ¥190 billion, all of which are expected to be record highs. For shareholder returns, we are guiding for an increase to the annual dividend per share of ¥5 from fiscal year ended March 2022 to ¥60.

Balance Sheet Control from a Medium- to Long-Term Perspective

As the Group's main businesses of real estate development and neighborhood creation-oriented businesses are characterized by the heavy long-term use of the balance sheet, balance sheet control from a medium- to long-term perspective is extremely important to achieve future earnings and profit growth and improve efficiency. Specifically, we take a 5 to 10 year perspective, combining proactive growth investments with cost recovery through continuous asset replacement in a well-balanced manner. We manage the entire balance sheet from a high level, through measures such as maintaining financial soundness through appropriate management of outstanding interest-bearing debt and the debt/equity ratio.

Looking back on balance sheet assets over the five-year period from the fiscal year ended March 31, 2017 to the fiscal year ended March 31, 2022, total assets increased approximately 1.5 times from ¥5,551.7 billion to ¥8,208.0 billion. This was mainly due to the successful conclusion of growth investments including successive completions of large-scale development projects in Hibiya and Nihonbashi, and the consolidation of the Tokyo Dome Group. While promoting growth investment, in recent years we

also engaged in asset turnover, such as selling Shinjuku Mitsui Building, Iidabashi Grand Bloom and Nakanoshima Mitsui Building to our sponsored REITs. Also, under the policy of reducing strategic shareholdings, we are trying to maintain and improve ROA by building a resilient asset portfolio.

The future external environment is expected to remain

increasingly uncertain, with inflation rising around the world due to factors such as supply chain and logistics disruptions and supply

constraints, and emerging risks such as rising interest rates. In such an environment, maintaining and building a sound financial

position is important for the stable continuation of business. For this purpose, the Group manages its balance sheet by keeping

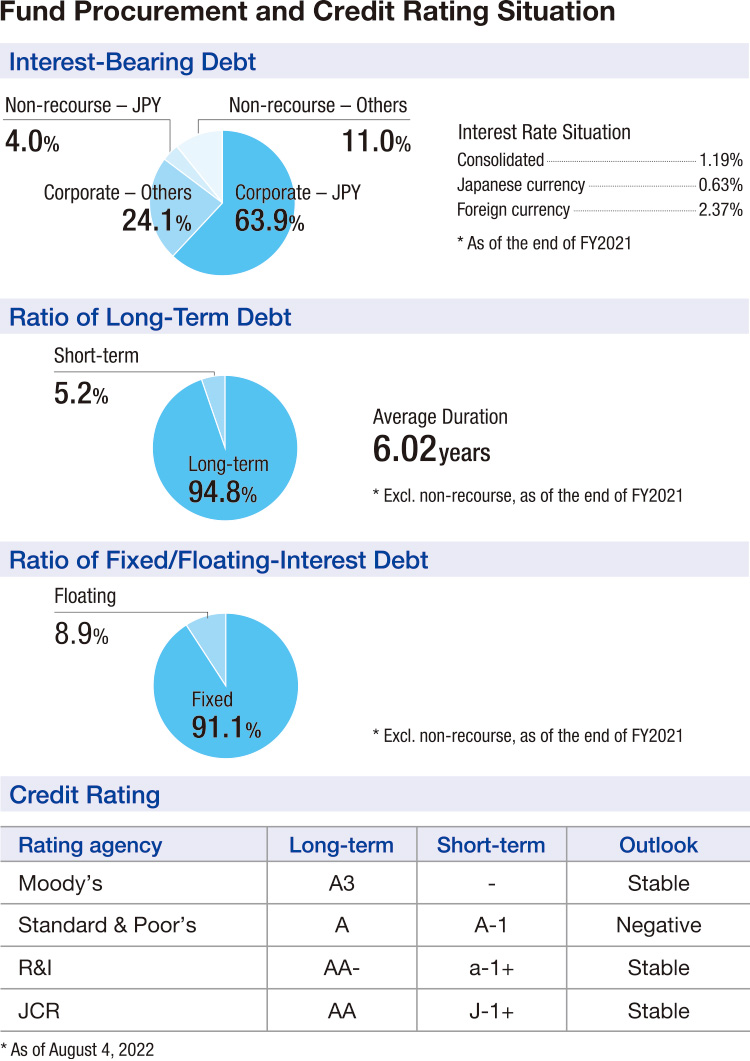

interest-bearing debt at about ¥4 trillion with a debt/equity ratio of about 1.2 to 1.5 times. At the same time, to reduce risks related to financial market volatility while property development projects are underway, we are taking measures such as raising the ratio of fixed interest rate borrowings and long-term borrowings, staggering repayment periods and maintaining our credit rating.

We have also secured commitment lines totaling ¥400 billion to maintain liquidity for emergencies. As part of funding actions in the

"Group Action Plan to Realize a Decarbonized Society" that we formulated in last autumn, we issued green bonds of ¥80 billion in

July this year, the largest amount ever issued by a domestic real estate company. As such we are striving to diversify funding sources as well. In addition, to prepare for exchange rate fluctuations, we work to offset and reduce risks by using natural hedges, mainly inoverseas businesses via fund procurement in local currencies.

Achieving Medium- to Long-Term Goals and Enhancing Our Corporate Value

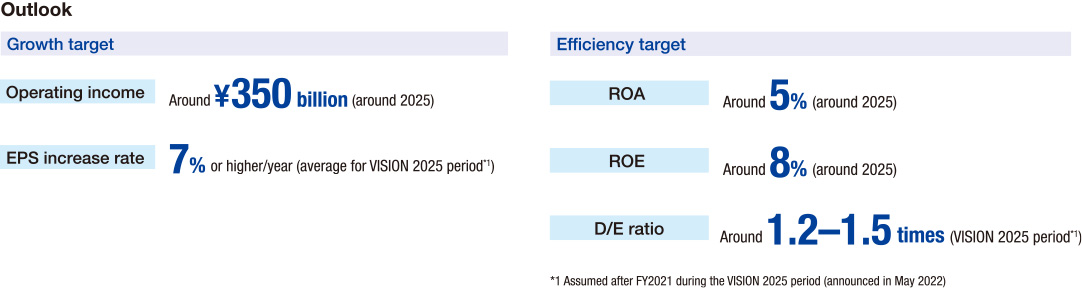

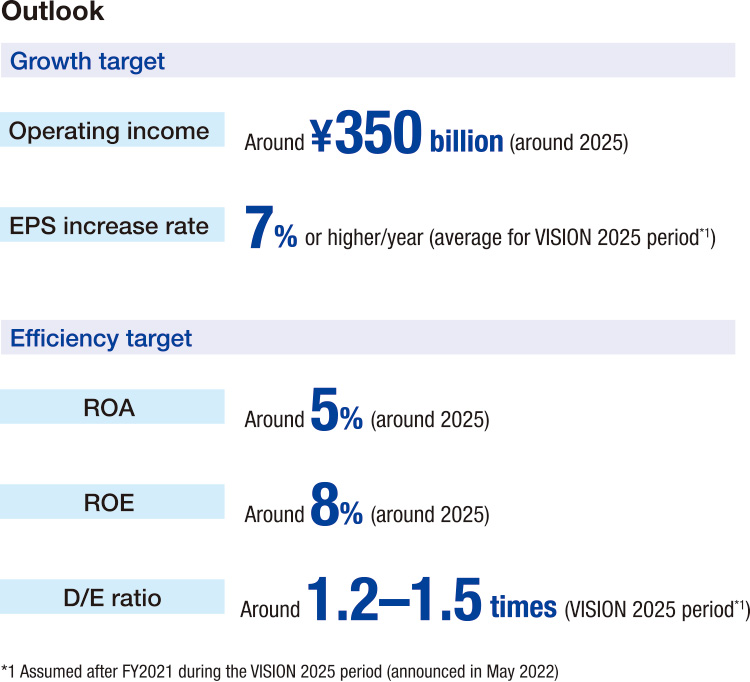

The Group's medium- to long-term growth targets are operating income of about ¥350 billion (around 2025), annual EPS growth rate of 7% or more (average up to 2025), and its efficiency targets are ROA of around 5% and ROE of around 8% (both around 2025).

Achieving these goals will not be easy in a rapidly changing external environment. However, we continue to see steady results from continuous investment in superior projects based on a solid financial position as well as progress on ongoing projects. As specific drivers of future profit growth, we expect to see a recovery from the impact of COVID-19, mainly at hotels and resorts and Tokyo Dome and normal operation and profit contributions from large-scale, mixed-use projects (TOKYO MIDTOWN YAESU and 50 Hudson Yards) which will be completed in fiscal 2022. In addition, assuming about 30% of assets under development and about 50% of central urban assets relative to total real estate assets, with a debt/equity ratio of about 1.2 to 1.5 times, we aim to further improve efficiency by promoting continuous balance sheet control. (See p. 33.)

We aim to achieve future earnings and profit growth and improve efficiency while staying abreast of the real estate cycle and interest rate trends. We will maintain our long-term financial strategy of investing selectively while being mindful of cost recovery and cash flow, and promoting balance sheet control with a focus on growth and efficiency. We believe this will allow us to consistently generate returns in excess of our cost of capital; we remain committed to further enhancing corporate value.